The screen business is consolidating around inventory. APAC will resolve it first.

If you have watched any premium streaming on a smart TV in the last year, you have probably seen them appear. A semi-transparent strip sliding along the bottom of the screen during the show. A squeezed-corner frame opening up space for a brand mark. A picture-in-picture box beside the action.

The formats are not new. What changed last week is that they now have a programmatic marketplace.

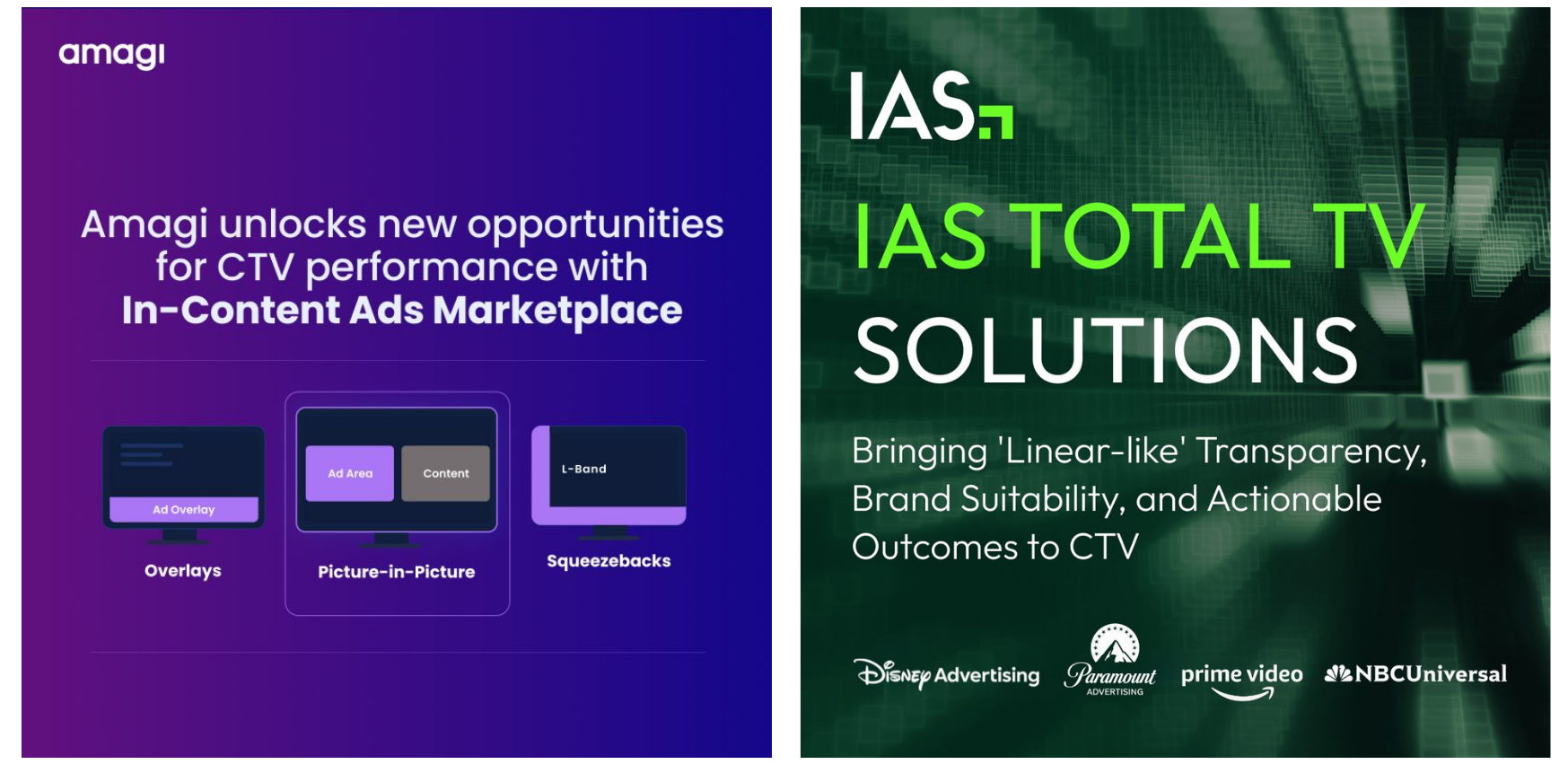

On 5 May 2026, Amagi opened its In-Content Ads Marketplace, making overlays, squeeze-backs, and picture-in-picture ads available at programmatic scale across hundreds of streaming channels.

Eight days earlier, IAS launched Total TV, giving advertisers show-level visibility into Disney, NBCUniversal, Paramount, and Prime Video, plus opted-in publishers using Publica.

Two ad-tech announcements eight days apart. Read separately, routine industry news. Read together, the same signal.

The infrastructure layer of television is consolidating around connected TV inventory as the unit of value. The competitive question is no longer which platform wins. It is who controls measurable, monetisable viewing inside connected environments, and at what price.

That sounds like an industry-trade observation. It is not. It changes which projects buyers will pay for, and at what rate, across the rest of the decade.

What the MPA numbers are actually saying

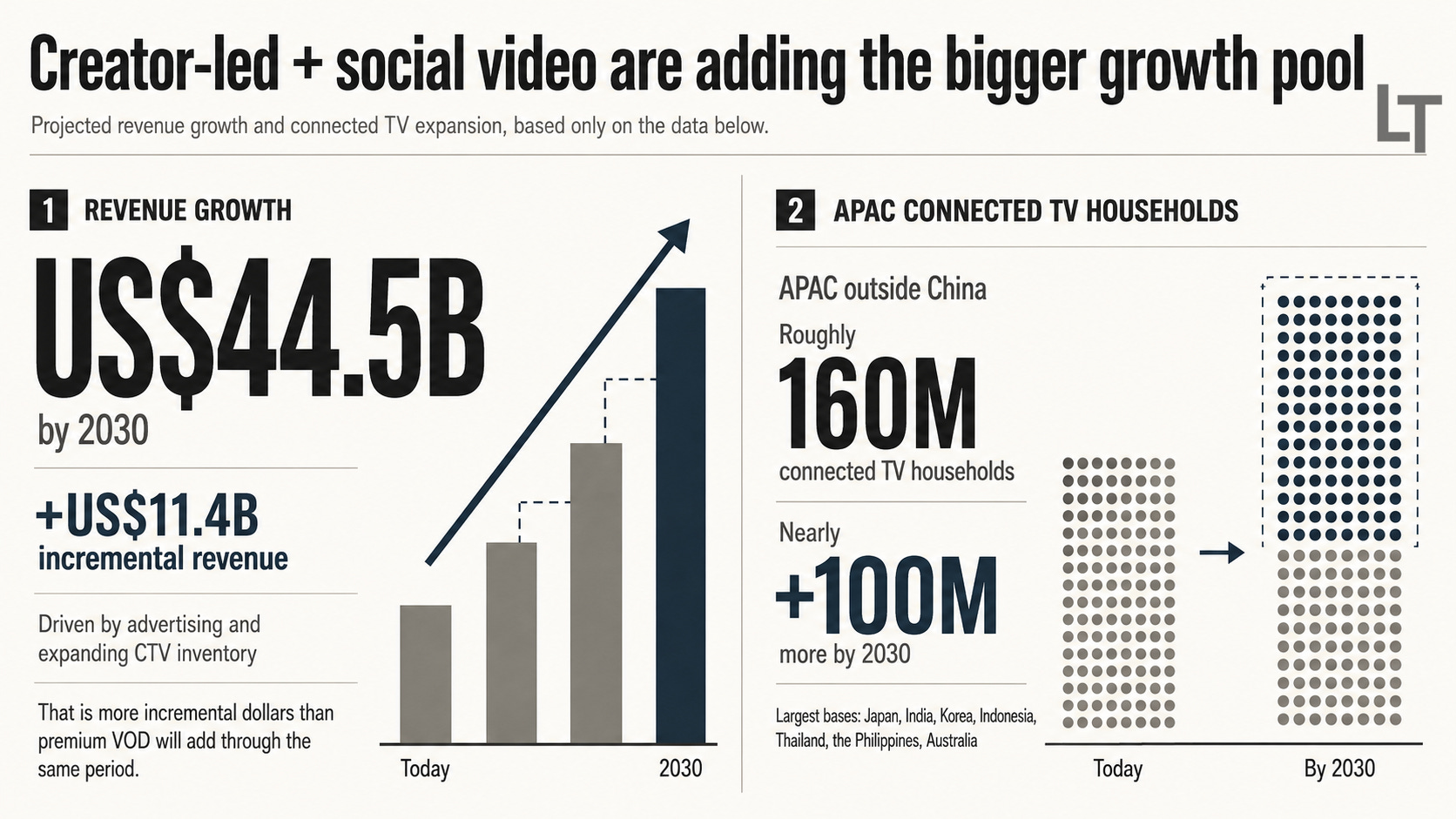

In January, Media Partners Asia released its Asia-Pacific Video and Broadband 2026 report. The headline stats made the trade press. Total APAC screen revenues will reach US$196 billion by 2030 at 2.8 percent CAGR. All net growth coming from online video. Traditional television revenues declining cumulatively by US$8 billion. India overtaking China in SVOD subscriptions, with 358 million by 2030.

Inside the report, the more important sentence sits in the framing. Vivek Couto, MPA’s CEO, describes the shift as value moving “decisively toward streaming, social platforms and CTV-led monetisation.”

The report identifies connected TV explicitly as a “structural driver of value creation” across the region.

The number that matters most is one that gets less attention. Creator-led and social video revenues are projected to add US$11.4 billion by 2030 to reach US$44.5 billion, driven by advertising and expanding CTV inventory. That is more incremental dollars than premium VOD will add through the same period. APAC outside China already has roughly 160 million connected TV households and will add nearly 100 million more by 2030, with the largest bases in Japan, India, Korea, Indonesia, Thailand, the Philippines, and Australia.

Set those numbers next to the Amagi and IAS launches. The pattern is not subtle. The infrastructure to monetise connected TV at television-grade economics is being built at the same time that connected TV is becoming the dominant viewing environment across the region.

This is the consolidation but not in ownership but in economics.

Why “creator vs streaming vs broadcast” is the wrong frame

The TV industry still argues about competitive position in old categories. Broadcasters versus streamers. Streamers versus social. Premium versus user-generated. Platform exclusivity versus open distribution.

The connected TV economy is, increasingly, indifferent to those categories.

A creator video watched on a phone behaves like social media inventory. It generates short, scrollable attention. CPMs reflect that. The same creator video watched through a smart TV interface in a living room behaves like television inventory. Longer sessions, lean-back attention, household co-viewing, stronger brand-safety conditions, higher CPM potential.

What changes is not the content but the buying system.

The Amagi product makes this concrete. Overlays and squeezebacks are not a streaming-first ad format. They are a television-grammar format being injected into streaming pods. The IAS product does the inverse. It applies television-style transparency expectations, programme-level, genre-level, ratings-level, to streaming inventory that has historically been bought with much less granularity. Both moves point in the same direction. Streaming is being made legible to advertisers in the categories television has long used. Television, meanwhile, is being measured by streaming-grade data.

The convergence is happening at the buying layer, and it is bringing creator content, sports streams, FAST channels, AVOD tiers, and ad-supported SVOD into the same monetisation architecture.

That is the consolidation. Different content, same inventory economics, the same buyers operating across the lot of it.

Why APAC will resolve this first

Three conditions matter, and APAC has them stacked.

The first is structural Average Revenue Per User (ARPU) pressure. Subscription economics alone cannot carry the cost base of premium streaming in lower-ARPU markets. India, Indonesia, Thailand, Vietnam, the Philippines. None of these support the per-subscriber economics that built Netflix’s first decade. Advertising-led monetisation is not a strategic preference here. It is a necessity.

The second is mobile-first viewing combined with rapid CTV adoption. The region jumped a generation of cable infrastructure. Audiences moved from broadcast to mobile to connected TV with less time spent in the linear pay-TV middle than the US or Europe. The MPA estimate of 100 million additional connected TV households by 2030 is concentrated in markets without the entrenched cable economics that elsewhere slow down inventory restructuring.

The third is platform fragmentation. APAC has more meaningful regional and national streaming players competing alongside global platforms. JioHotstar in India, U-NEXT in Japan, Stan and Binge in Australia, Viu and iQiyi across Southeast Asia. None of them can defend their economics through global scale alone, which forces them earlier into ad-supported tiers, FAST channels, hybrid bundles, sports rights gambits, and creator partnerships.

Combined, those conditions push APAC toward the connected TV inventory model faster than the US or Europe will be pushed.

What this means for projects

The version of this story I keep encountering inside development conversations is “streaming is hard, the buyers are cautious, projects keep getting deferred.” That reading is not wrong. It is incomplete.

The deferrals are the symptom. The cause is that the underlying buying logic is changing, and projects packaged for the old logic look misshapen in the new one.

In the scarcity-era model, project value came from prestige, exclusivity, and the ability to spike subscriber acquisition. That model still exists, especially for tentpole drama. But the additional value layers being built around connected TV inventory reward different qualities. Repeatable engagement that compounds across viewing systems. Formats that travel into FAST channels and AVOD tiers without losing their economics. Returnable architectures that keep generating measurable inventory after the launch window. Local-language premium content that anchors connected TV households inside specific markets.

Rights-side, the implications are sharper. Exclusivity-led packaging assumed that holding a project off the open market raised its price. In an inventory economy, holding something exclusive can also remove it from the buying systems where its monetisation actually compounds. Rights flexibility, multi-window structures, and clean ad-integration permissions are starting to matter more in deal value than they did three years ago.

For brand-content leads, the shift cuts the other way. Brand-funded content that lives only on owned channels is competing against the same connected TV inventory pool, often with worse measurement. The arbitrage that brand content used to enjoy, cheaper than TV, more controllable than streaming, is narrowing as connected TV measurement closes the transparency gap.

The misread to avoid

The industry keeps calling this moment fragmentation. The word fits the surface. More platforms, more formats, more partners, more contracts.

The economic substance is the opposite. Underneath the surface fragmentation, the buying systems are consolidating around fewer, larger architectures. Demand-side platforms. Connected TV measurement standards. Programmatic supply infrastructure. Inventory marketplaces.

The companies winning the next decade will not be the ones with the most content. They will be the ones whose content sits inside the most efficient connected viewing environments, with the cleanest measurement, the most consistent ad-load economics, and the fewest barriers between an audience hour and a monetisable impression.

For producers and rights holders working in APAC, the question for the next packaging cycle is not “which streamer should I target.” It is whether the project is being built to generate monetisable connected TV viewing at the rate its production cost requires, and whether the rights structure preserves that monetisation across the full life of the content.

Most slates currently in development do not yet pass that test. They were packaged for the previous market.

The buyers, increasingly, are operating in the next one.

If you are sitting with a version of this problem on a live project and want a clear outside read before more time goes into the wrong direction, send a short note describing the situation to adi.tiwary08@gmail.com. I take a small number of these each quarter.

Sources

Media Partners Asia, Asia-Pacific Video and Broadband 2026 report, January 2026.

The Hollywood Reporter, “Asia-Pacific Video Revenue to Reach $196 Billion by 2030, Driven by Streaming and Social,” January 2026.

IAS / BusinessWire, “IAS Launches IAS Total TV Solutions Giving Marketers ‘Linear-like’ Transparency for Connected TV,” 27 April 2026.

Good piece